The UK’s population is expected to grow by almost 10 million in the next 25 years putting considerable strain on energy, transport systems, water and social infrastructure. With this in mind, there is a need for an explosion of infrastructure development across the country. What does this mean for the role of the general counsel involved with infrastructure projects, and what are their main challenges?

The UK’s population is expected to grow by almost 10 million in the next 25 years putting considerable strain on energy, transport systems, water and social infrastructure. With this in mind, there is a need for an explosion of infrastructure development across the country. What does this mean for the role of the general counsel involved with infrastructure projects, and what are their main challenges?

Mark Richards, BLP: Brexit seems tied into the potential long-term planning of UK infrastructure, UK growth, industrial strategy, regional growth, rebalancing the economy, London vs the rest of the country – these are all big topics for infrastructure generally. How is Brexit affecting you, or is it business as usual?

Mark Richards, BLP: Brexit seems tied into the potential long-term planning of UK infrastructure, UK growth, industrial strategy, regional growth, rebalancing the economy, London vs the rest of the country – these are all big topics for infrastructure generally. How is Brexit affecting you, or is it business as usual?

Mark Noble, National Grid: We were halfway through a deal [the sale of 61 per cent of the gas distribution business to a Macquarie-led consortium] at the time of the referendum, and like everybody else, we were unsure what the impact would be. In fact, through the work of our fantastic treasury colleagues, we found it the perfect time to issue a huge amount of debt.

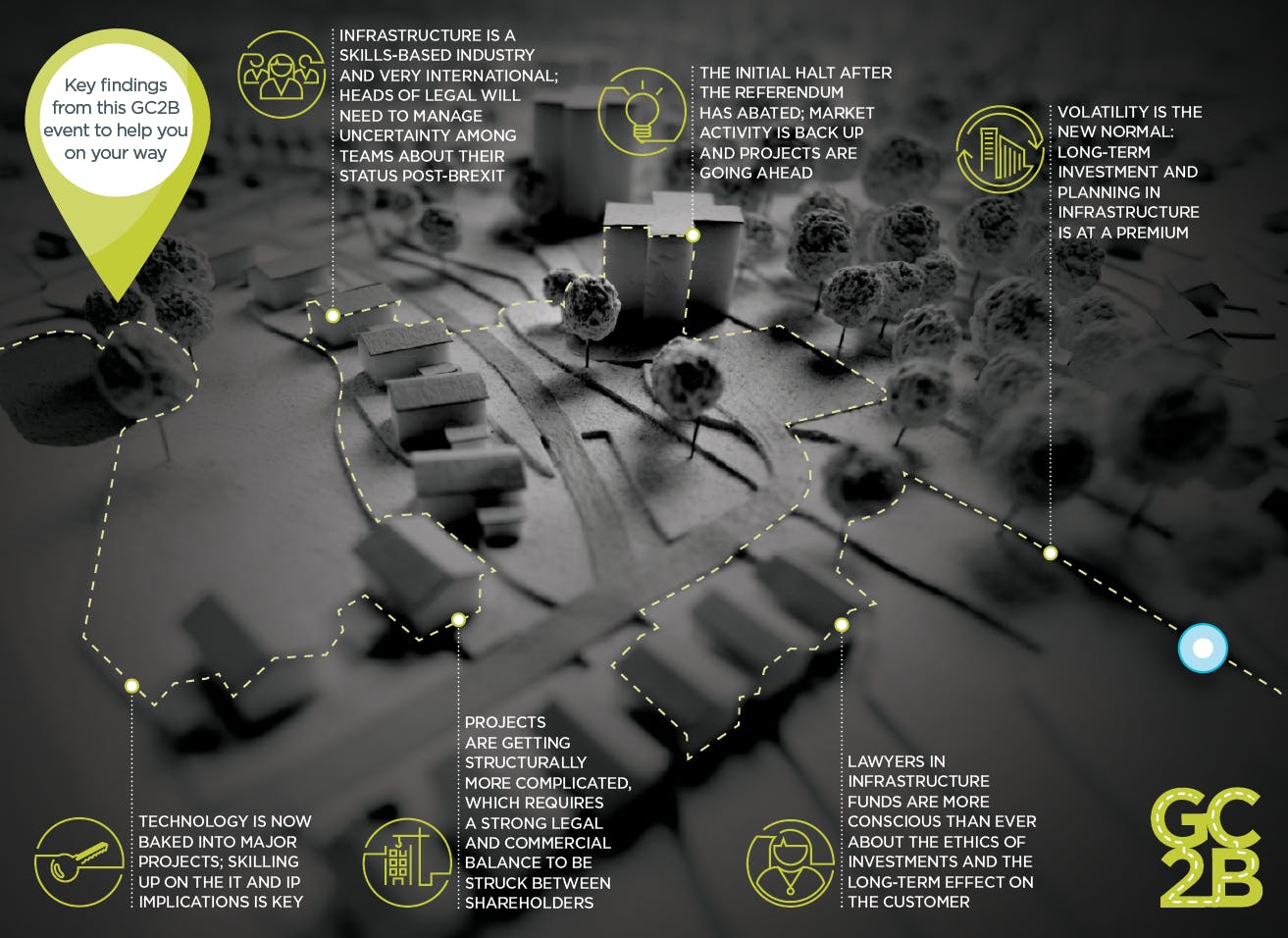

Tracey Lee, Tideway: We were lucky in that the referendum kicked off after financial close for us. The biggest concern that keeps us awake now is skills – a reduction of skilled people as a result of the chain of construction changes moving down the supply chain.

Mark Richards, BLP: One of these issues leading the conversation is skills. Is that a concern going forward?

Jim Stoner, 3i: Over half of our team are international – from Europe, Australia, the US and elsewhere – and they were genuinely worried to start with. Our employment team has been reassuring them so far as they can that nothing is going to change.

Jilly Ward, Atkins: From an engineering point of view there is a skills shortage anyway, and there is only so much reassurance you can give as an employer. I think there is going to be an interesting fall-out.

“There is a skills shortage in engineering anyway… I think there is going to be a fall-out from Brexit”

Jilly Ward, Atkins

Paul Starkey, Costain: Getting and retaining good people has always been a key challenge. We’ve got people from all over the world and anything that makes them less certain about their career in the UK is not positive.

Equally, we’re doing a lot of work to bring trainees into the business. When I first joined the legal team at Costain, it was hopelessly top heavy. Now we’re a much more balanced team. One of the solicitors used to be a PA who did their training, and we’ve got another paralegal who is hopefully going to start a training contract with us.

With engineers, it’s not so much the company they work for necessarily, but whether they can get the iconic engineering projects.

Mark Richards, BLP: How do you manage political risks with your investors and your clients?

Ece Gursoy, Lightsource Renewables: So far our investors are UK-based so we are looking at the same risk investments. We took Brexit from a different angle: whatever the outcome, the country would still need energy, and if the electricity prices are going up, solar is a very easy source to develop for decent energy results.

“We have 25 nationalities in our company; on the day of the Brexit result, there was a very gloomy mood about the future of these young talented people”

Ece Gursoy, Lightsource Renewable Energy

From the talent point of view, in our company we have 25 different nationalities. On the day of the Brexit result, there was a very gloomy mood in the office about what these young talented people will do. In my own team at some point we had 27 lawyers, half of them foreigners with UK qualification and the other half leading lawyers from their own jurisdiction.

Mark Sanderson, Severfield: The mood at the moment is very positive but the challenge as a plc is that you are required to identify and comment on any potential Brexit-related risks to your business. So we did a lot of head-scratching to try to look around corners and work out potential problems.

There was a major skyscraper in the City – 22 Bishopsgate, which used to be called the Pinnacle – that was to be redesigned. We all thought the project would be cancelled soon after the Brexit vote, but it wasn’t. They postponed the decision for two or three months but then decided to proceed, and for me that was a positive sign. As a result of that, we don’t see a downside. Obviously the market will turn, which is where infrastructure for us will step in to cushion us from any shocks in the commercial retail markets. A lot of our market is big distribution warehouses and shopping centres and skyscrapers.

Katherine Laurenson, Legal & General Investment: For us the challenge is finding those projects that are structured or can be structured in a way that attracts institutional money like us and stick with it for the long term.

John Broadhead, Atkins: Clearly Brexit is an obstacle to the way in which money is going to find its way to infrastructure. We need to find a way to get it moving in the right direction.

Mandeep Mundae, IFM Investors: A lot of our investors are concerned about the outcome of the referendum, particularly those linked to GDP. There was an immediate question mark for example, on what it means for airports. Investors understand there is an uncertainty and they will stick with it to realise the long-term goals for capital rather than the short-term ones.

Ian Crawley, Aviva Investors: There is a need across Europe, not just the UK, for infrastructure projects. If you’ve got an investment base that is looking for long-term stability then Brexit will have an impact, but I think it will be a short sharp impact. Once everybody figures out what the actual ramifications are, the projects that need to be done will get done.

“Brexit will have an impact, but I think it will be a short sharp impact… the projects that need to be done will get done”

Ian Crawley, Aviva Investors

Mark Richards, BLP: It was a reportedly quiet July and August for commercial real estate but we are seeing volumes pick up since then and we are back to where we were. In terms of infrastructure I’ve never seen so much M&A in the market. It’s very busy at the moment.

We are talking to clients about macro Brexit issues but in terms of particular advice and the issues – we’ve had a small number of financial institution mandates about possible relocation but nothing further than that.

“The infrastructure markets are getting a bit more shockproof. There was an initial dip after Brexit but a really strong recovery”

Mark Sanderson, Severfield

Mark Sanderson, Severfield: What is encouraging is that the markets are getting a bit more shockproof. There was an initial dip after Brexit but a really strong recovery. The same is true after Trump’s election – an initial dip then strong recovery. There was a time four to five years ago when the market couldn’t sustain any one of those drops. That suggests investors are willing to accept that there is a new normal out there, which is a less certain world.

Katherine Laurenson, Legal & General Investment: People understand what real value is now. They’re looking at the financials.

Mark Noble, National Grid: There’s a limited number of asset classes you can invest in. Bonds are not exactly shelling out a vast amount of interest. But I accept your point, people have got used to seismic change and are digesting it.

Mark Richards, BLP: Infrastructure projects are traditionally complex, especially in London. These projects are not getting simpler, are they?

Paul Starkey, Costain: No they’re not, and what’s more, they’re getting bigger. There’s collaboration between the funders and the SPV that delivers it and the stakeholders who do the work on the project. If you can get the three of them working together you get the best project solution. Otherwise you can spend a lot of time debating who is going to take the risk instead of what’s best for the project.

Katherine Laurenson, Legal & General Investment: Do you see the lawyers pre-empting that and providing legal advice that solves that?

Paul Starkey, Costain: It varies, if I’m being honest I’m not sure how much the lawyers are in control of these things. These deals are hugely complicated, enormous, long-term, multi-stakeholder, nationally important projects. They will still get done but they are complicated enough without lawyers trying to score points. You need a risk mix that works for all the parties because if someone has a bad day it’s a bad day for the project.

Mark Richards, BLP: Are there any lessons that can be learned from collaborating and working together?

Tracey Lee, Tideway: The Tideway is a project that took a decade to get planning. We were negotiating with the government and Ofwat and the construction contractors for three or four years to develop the structure. There is an inherent fear of being innovative – we tend to do what we’ve done before. So our starting point is ‘what did they do on Crossrail, what did they do on the London Olympics’? We all create the same structure and security packages because so much is at stake.

“The biggest concern that keeps us awake about Brexit is a reduction of skilled people as a result of the chain of construction changes”

Tracey Lee, Tideway

Mark Richards, BLP: Isn’t part of the role of an in-house lawyer in the infrastructure sector to bring some innovation?

Tracey Lee, Tideway: As an in-house lawyer it’s a constant challenge. Your role is to provide legal advice to all of your clients in the business but at the same time you must balance that with commerciality. When you sit in front of your board and say, this is innovative but we don’t really need it and this is the belts and braces, you can bet your bottom dollar they will go for belts and braces.

Ian Crawley, Aviva Investors: As the in-house lawyer, you’ve got the remit to challenge the lawyers you’ve appointed.

Catrin Griffiths, The Lawyer: To what extent do you have your ears to the ground about new structures and new ideas around that? If you want to know what is going on in another projects, would you call your private practice lawyers or do you have a network you can pick up the phone to?

Tracey Lee, Tideway: I wouldn’t say it’s fully developed or formalised, but we do pick up the phone if we want to understand something.

Jilly Ward, Atkins: I agree. You rely on your own professional network and the people you know to benchmark and form ideas. There is also paranoia about competition and what you can and can’t say and it’s probably easier not to say anything at all.

Catrin Griffiths, The Lawyer: The reason I ask is that we’re doing a project around the Disruptive GCs network, who are sharing industry experience with one another and cutting out private practice. It’s an interesting way of sharing knowledge and building a comradely feeling. How transferable is that to other sectors?

Jilly Ward, Atkins: I think it’s definitely transferable, but one of the issues is the effort involved. If you’re already in that agile environment it’s easier I think, whereas we come from a very conservative environment. I’ve always thought it would be particularly useful for consultants in my sector to get together because we tend to get the bad end of the stick when it comes to contracting and the risks we have to take. I think it is a matter of paranoia about competition law and what you can and can’t share. It would be helpful to have a more collaborative view about the risk you are willing to take.

Jim Stoner, 3i: When you need some information, say about electricity and interconnector investments, we have to turn to the law firms and financial advisers for information about the deals they have done in that space, so they are still really important for that information.

Mark Richards, BLP: How much relevance do some of the things you see in the press about legal technology have on your day to day lives as infrastructure GCs?

Ian Crawley, Aviva Investors: The interesting point is how it affects the service providers that we get services from. Increasingly there is a lot of pressure on the bottom line, there needs to be a justification for fees and how can technology assist us for getting what we need for the business.

Mark Richards, BLP: If the legal industry is willing to change its service model, how will you change your models internally to accommodate these new services?

Mark Noble, National Grid: I think we have to change we have no choice. Infrastructure projects end up being multi-faceted with multiple law firms. We are funded by our taxpayers so we have to demonstrate we are doing the best by managing our business.

Catrin Griffiths, The Lawyer: Given the changes that technology is creating in terms of smart materials, what does that mean for you in terms of risk profile?

Paul Starkey, Costain: It goes back to customers expecting a different product. It’s not just about a bridge, it’s about a bridge that can have some technology built into it that will sense additional weight on it and technology that tells you when it needs to be serviced. It’s a really big issue. We’ve acquired a couple of businesses recently that have technology solutions particularly in the highway sector. We bought a business last year that had some incredible CCTV cameras – they’re a given now if you’re working on a highway job.

Mark Sanderson, Severfield: It is a challenge for us in terms of risk transfer. The more we are involved in providing modular solutions or technology-rich solutions then you’re coming up against different players in the supply chain who aren’t familiar with the same risk transfer model.

Paul Starkey, Costain: I agree. Say we collaborate with a specialist with particular software and help introduce that into one of our projects where perhaps it’s not used in that current market. Then we have the issue of who will develop the software together.

Mark Sanderson, Severfield: You need high levels of collaboration, high incentives for innovation and you need a definite contracting model.

Jilly Ward, Atkins: Historically we’ve seen ourselves as a design house and we’ve given away a lot of our intellectual property, but I think there is going to have to be a change in the contracting mindset. We’re investing heavily in the digital sector.

Mark Richards, BLP: What does the infrastructure lawyer of the future look like in-house?

Jilly Ward, Atkins: One of the obvious things is I’m going to have to upscale my team on IP and different commercial models. There might even be borrowing of ideas from other sectors you wouldn’t expect, such as retail, which sell subscription services, for example. We’re going to have to be more innovative.

Katherine Laurenson, Legal & General Investment: The in-house lawyer in infrastructure is already required to be intellectually flexible.

Ece Gursoy, Lightsource Renewable: Your legal knowledge and skills are there; what you need to know is the business to distinguish you from the external counsel.

Ian Crawley, Aviva Investors: I think the role continues to be the same but it becomes a little harder as you have to be the bastion of conscience for what is going on. So for us investing pension fund money, I am always conscious of the end customer – what would they think about where you’re going? Over the coming years and decades, infrastructure and what we think it is today will change, and people will want to invest in it and as an in-house lawyer you have to say, yes invest but also look at the risks. We need to keep that conscience and speak up. You may be overruled by your committee or by the teams, but as long as you’re implementing that conscience of challenge, that’s what is needed.

GC2B is an initiative from The Lawyer and Berwin Leighton Paisner

Mutual benefit: GC = business

GC2B run regular roundtable events discussing the current issues affecting in-house lawyers. To join the debate, attend an event or for more information, contact emma.bower@centaurmedia.com