What do Syngenta, Pentair and Gategroup have in common? They are all Swiss-headquartered companies that have been sold for billions in the past year.

The Syngenta and Pentair deals are yet to be completed but the trend is clear – Swiss corporates are attractive to international buyers, particularly from China and North America. Meanwhile, M&A activity between Swiss companies and European rivals remains buoyant.

Reasons for the trend include Switzerland’s strength in the technology and pharmaceuticals industries, steady cashflows and solid management. Also, minimal barriers exist to prevent foreign buyers wading in.

While many of the headlines have been taken up by China National Chemical Corporation’s (ChemChina) $46.6bn (£38bn) purchase of Syngenta a steady number of deals are being announced in the small- to mid-market arena, both cross-border and domestic. These feature Swiss companies such as Lonza, INEOS and Swiss Re.

The Swiss market is certainly one to watch in 2017, with countless opportunities opening up for the region’s firms. And whether they win work through local relationships or international referrals, Swiss firms will play an important role on the global M&A scene too.

The Lawyer asked some leading lawyers in the country for their thoughts on M&A trends.

Q: Are you seeing more cross-border M&A deals out of Switzerland? If so, why do you think this is?

Catrina Luchsinger Gaehwiler, partner, Froriep: In our experience most M&A transactions relate to privately-held targets, when owners decide to sell their companies.

While we do not see an increase in dealflow it is interesting to note that there is still a steady flow of small- to mid-market sized cross-border deals, notwithstanding the strength of the Swiss franc [CHF].

What makes Switzerland an interesting place for acquirers is its strength in R&D in the biotech and high-tech industries. This has created numerous specialised but important niche-players. Their revenues have, in many cases, been robust as their products are not easily replaceable.

Philippe Weber, partner, Niederer Kraft & Frey: In recent years there have been a number of important cross-border M&A deals out of Switzerland. These include the $25bn asset swap between GlaxoSmithKline (GSK) and Novartis and the acquisition of Orange Communications by French telecoms tycoon Xavier Niel for CHF2.8bn (£2.3bn). Other deals include the combination between Lafarge and Holcim, the takeover of Syngenta by ChemChina and, most recently, the $30bn takeover bid of Johnson & Johnson (J&J) for Actelion.

Swiss companies are well-managed and often have strong international market positions, constant cashflows and attractive IP portfolios. At the same time, the legal, regulatory and financing environment in Switzerland is benign and stable. For example, apart from a few regulated areas (such as financial services and residential real estate) there are basically no barriers for foreign buyers.

“The legal, regulatory and financing environment is benign and stable” Philippe Weber

Also, Swiss companies and their management typically are internationally minded, which makes integrating and partnering with them easier.

Daniel Daeniker, managing partner, Homburger: In our day-to-day business, cross-border deals account for more than 50 per cent of overall M&A volume. This is easily understandable, given the vast international outreach of Swiss companies of any size, the trade flows between Switzerland and the rest of the world and the relative smallness of the Swiss market.

In 2016/17, we have seen a few prominent big-ticket M&A transactions, most importantly the takeover of Syngenta by ChemChina and the takeover of Actelion by J&J. But this is more a sign of a mature M&A cycle than a trend that would be arcane to Switzerland.

Mariel Hoch, partner, Bär & Karrer: After a strong year in 2014 M&A activity slowed in 2015. While the number of deals increased a little in 2016, the second-highest deal volume since 2007 has now been reached.

Some reasons for the hesitation of investors include the implications of the decision of the Swiss National Bank to discontinue the minimum exchange rate of CHF1.20 per euro and political uncertainties such as the decision of Great Britain to leave the EU and the US presidential election.

“Reasons for investor hesitation include the end of the CHF1.20 per euro exchange rate” Mariel Hoch

At the same time, generally low financing costs have supported transaction volume but the largest contributor to deal volume was the deal between Syngenta and ChemChina, which marks the largest transaction in the history of Switzerland. We expect a strong year for cross-border M&A.

Q: What trends are you seeing in the types of deals being announced?

Daeniker: As noted, we are seeing more big-ticket transactions, which is fairly typical for the maturity (and near-end) of an M&A cycle.

Gaehwiler: We still see the bulk of the transactions being small- to mid-sized. High-profile public takeovers remain scarce, not least as there is often a controlling shareholder who first needs to be convinced to sell out.

Weber: Transactions are becoming more complex, both structurally and finance-wise. A good example is the recently announced takeover bid of J&J for Actelion, which combines the public takeover of Actelion with the spin-off and listing of Actelion’s research and early stage clinical development pipeline. This is a novelty – the first of its kind in structure.

Factors affecting the complexity of cross-border deals are often international taxation and regulation, which have become increasingly complex and difficult to reconcile, especially when multiple jurisdictions are involved as is typically the case with Swiss-headquartered targets.

Another trend is the need for more due diligence in compliance matters such as in the areas of sanctions, bribery and competition, where multibillion-dollar fines and the withdrawal of business licenses have become the reality not only in the US but globally.

Accordingly, before they buy another company clients need to be comfortable that they are not ‘buying a problem’. This often affects not only the level of due diligence but also the way a deal is structured. For example, if a bank wishes to buy another bank a more complex asset deal may, on balance, be better because it allows the buyer to carve out undesirable risk.

Hoch: In 2016 Chinese investors made more acquisitions in Switzerland and Europe than in any previous year. For the first time China’s outbound M&A activity in Switzerland overtook that of the US.

While most M&A deals took place in Germany and the UK, the highest transaction value was seen in Switzerland, mainly due to the Syngenta transaction.

The trend of Chinese investment in Swiss industrials has become manifest in the acquisitions of Gategroup, SIGG Switzerland and Acino Supply. We expect this trend to continue in 2017 and further significant transactions may be expected in the chemicals sector as well as the industrial markets.

Chinese investments have so far proved to be stable and seem long-term-oriented. The steady growth of private equity-sponsored deals in Switzerland continued in 2016. The acquisition of the Kuoni group by EQT underlined the fact that public M&A is a new field for international private equity in Switzerland.

Q: How does your firm go about winning these mandates?

Gaehwiler: The Froriep partners who deal with M&A transactions have specialised niche areas or industry segments in which they are known among their peers and in the business community, be it on the start-up scene, real estate companies, the financial market, biotech or the sports world. This enables the partners to understand the interests of the parties involved, address the risks of the segment and provide advice that goes beyond the actual transactional work.

Weber: Our motto is ‘good work generates more work’. Therefore, while we regularly meet with clients and referral firms outside of client matters, we believe the best way to win mandates is to deliver quality work and client satisfaction.

Accordingly, a lot of our work comes from existing clients and top-tier foreign referral firms with whom we have longstanding working relationships. We generate the larger part of our M&A assignments from existing clients.

Thus our strong record continues to be a major business driver. In times of complex deals and short timetables clients are looking at law firms with up-to-date experience. Likewise, when asked, the banks and other financial advisers typically recommend the law firms with whom they have worked successfully most recently. Such an environment favours established players and makes it difficult for newcomers.

“Financial advisers typically recommend the law firms with whom they have worked successfully most recently” Catrina Luchsinger Gaehwiler

Market recognition is also important, especially to foreign clients and referral firms. The Swiss legal market is relatively small and clients typically will not entrust a lower tier firm with a high-end matter.

Another related factor is industry experience. For example, M&A partner Philipp Haas was Swiss counsel to GSK in the 2014 $25bn asset swap deal with Novartis. In the recently announced $30bn takeover bid for Actelion by J&J Haas and his team are acting as lead counsel to Actelion. Other industry sectors where we have built a strong reputation are financial services, TMT and private equity.

Daeniker: Most of our mandates are won directly from the companies instructing us. ‘Best friends’ referrals are important in connection with doing the Swiss aspects of an international transaction where the centre of gravity is outside Switzerland.

Hoch: Bär & Karrer has a wide network of international and domestic connections with partner law firms as well as long-term clients. Clients have access to a full range of legal and tax services, and we strive to be a Swiss pioneer on an international level. Our close and long-term collaboration with international partner firms also allows us to provide clients with legal advice in highly complex international transactions.

Q: What effect have high-value M&A deals had on the Swiss market?

Gaehwiler: They have put Switzerland in the limelight, showcasing the fact that the Swiss market has interesting targets. We are seeing more buy-side requests to find targets in various industry sectors. However, as companies are often privately held, finding approachable targets can be difficult.

Weber: These deals have lifted some Swiss firms to impressively high positions in international M&A league tables. The trend has also helped strengthen the international reputation of Swiss firms. In turn, it has probably widened the gap between the tier one and lower tier firms not only in terms of deal volume but also, for example, in their attractiveness as employers.

At the same time it has led to increased interest from international law firms. Thus far, most international firms have resisted opening an office in Switzerland but this may change.

At the same time it has led to increased interest from international law firms. Thus far, most international firms have resisted opening an office in Switzerland but this may change.

Daeniker: As always, these transactions are a sign that the Swiss M&A and capital markets are still active. Switzerland has traditionally been an open country so that there is hardly ever a political backlash about Swiss companies being taken over by foreign suitors.

Hoch: Certain high-value M&A deals have been associated with concerns about job cuts, relocation of production facilities or loss of independence of Swiss key industries.

However, recent high-value deals did not confirm those concerns. In particular, Chinese investors seem more interested in maintaining standards and leadership as a way of developing the Chinese market and exploring new areas.

Generally, high-value M&A deals lead to new industry giants and typically force local competitors to focus on niche markets and innovative technologies. In particular, smaller players will reinvent and reinforce their activities, especially through bolt-on acquisitions.

Q: What measures are you taking to ensure you stand out compared with your local peers?

Weber: We don’t measure ourselves against local peers alone. Indeed, while smaller in size we have the ambition to provide the same level of service and quality as tier one firms in the UK and the US.

To accomplish this we have invested a lot in recent years in IT. We recently introduced a data management system and will launch a new billing system this month. In 2017 we plan to introduce a client relationship management system, with all systems meeting international standards.

“We are seeing more big-ticket transactions, which is fairly typical of a mature M&A cycle” Daniel Daeniker

We were one of the first tier one firms to employ a full-time chief operating officer and further management initiatives are on the way. We are the only tier one firm located at the heart of the financial district in Zurich and we’re moving to a new landmark building in the same district in 2018.

While we do only practice Swiss law we have decided to hire non-Swiss lawyers from top tier foreign firms. We employ a significant number of US, UK, German and Italian lawyers who joined from firms such as Latham & Watkins, Kirkland & Ellis, Jones Day and Gianni Origoni Grippo Cappelli & Partners. This distinguishes us from other Swiss law firms and has strengthened our reputation in cross-border M&A and capital markets, where knowledge of international market practice is key.

We’re also strongly committed to gender diversity. A few years back we introduced a part-time female partner model and in the past two years we have promoted four female partners, two of whom have been on this part-time model.

Hoch: Efficient knowledge management and keeping track of local or global changes in legal frameworks as well as technological developments are increasingly important for us.

We strive to give our employees advanced training and education, and constantly improve our local and global network of specialised groups and partners to guarantee tailored advice for complex issues. As the expectations of clients are rising, a traditional training and education limited to legal contents is no longer sufficient. Given the international complexity and clients’ demands our specialists aim to provide quality solutions on all levels, round the clock.

Gaehwiler: Unlike other Swiss law firms Froriep’s client base is mostly foreign. With offices in London and Madrid, cross-border deals have always made up the majority of our workload so catering for clients outside Switzerland comes naturally to us. The combination of cultural diversity and sector-specialised knowledge in our M&A teams gives us an international flair that has been our value-add to foreign clients seeking to do business in Switzerland. This strategy continues to be vindicated by steady instructions on the M&A side.

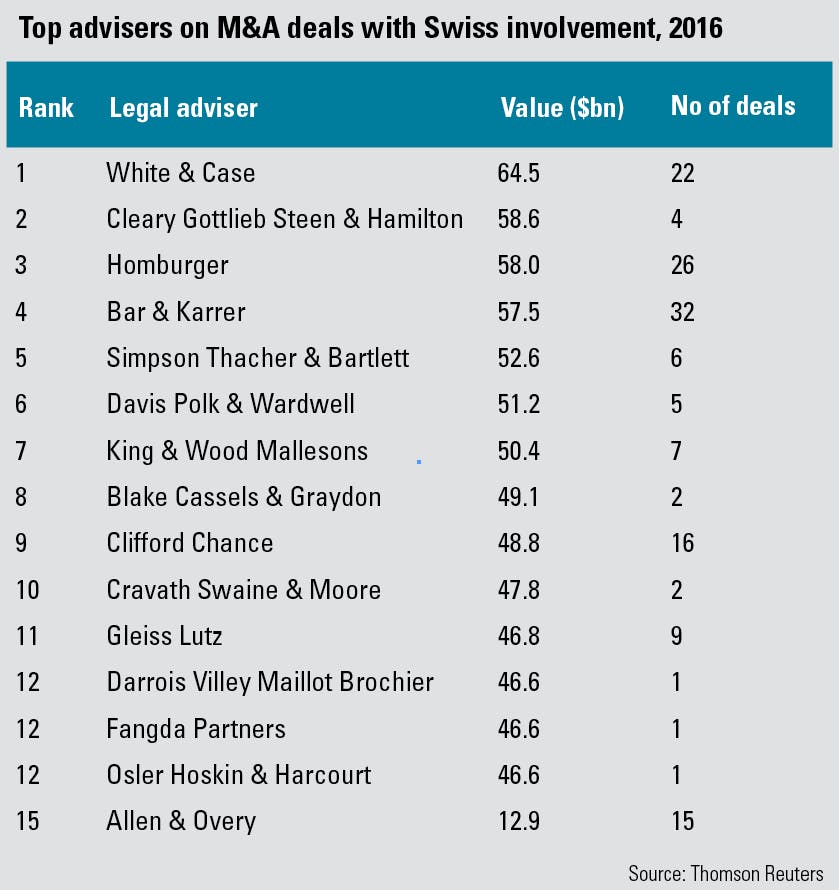

Biggest deals in the Swiss market in 2016

While Swiss firms played a vital role in many of the country’s largest deals it was White & Case that led the way as the nation’s top legal adviser for 2016. According to Thomson Reuters, the US firm worked on 22 deals with Swiss involvement with a value totalling $64.5bn. In second place was Cleary Gottlieb Steen & Hamilton, which acted on just four deals, worth $58.6bn.

White & Case won mandates on the three largest Swiss-related deals –Syngenta’s purchase of ChemChina, Lonza’s acquisition of Capsugel and QHG’s deal with NK Rosneft. The first two saw Swiss firm Homburger take the lead mandates on the domestic side. Bär & Karrer acted alongside Homburger on the Lonza deal amid a raft of UK and US firms such as Allen & Overy, Herbert Smith Freehills and Simpson Thacher & Bartlett.

Homburger and Bär & Karrer were ranked third and fourth respectively in terms of 2016 deals. US and UK firms feature prominently on the table, as does German firm Gleiss Lutz and French outfit Darrois Villey Maillot Brochier. Due to the heavy involvement of Chinese acquirers, Asian outlets such as Fangda Partners are counted among the 15 most active advisers on Swiss-related deals. In reality, Fangda acted on just one deal last year, advising ChemChina on its play for Syngenta.

The table does not take into account J&J’s proposed takeover of Actelion. Slaughter and May bagged a role for Actelion alongside Nieder Kraft & Frey. The acquirer is meanwhile seeking advice from Cravath Swaine & Moore, Homburger and SextonRiley.

The deal will see J&J acquire biotechnology company Actelion for $30bn. As part of the transaction, Actelion will spin out its research and development unit into a new Swiss biopharmaceutical company.

{kind=link}