New York is the world’s richest, biggest and most important legal market. Fact. Of the firms included in the market’s first-ever Global 200 ranking, which features firms from 94 countries and an astonishing 571 cities, 138 have an office in New York – more than any other. The shoo-in for second place? London.

Click here to view The Lawyer Global 200 2016 report

London is represented by well over half (122) of the Global 200 firms. And although there are 136 firms in the ranking with offices in Washington DC, and indeed the US’s capital city is home to precisely eight more partners than its UK counterpart (5,355 to London’s 5,347; New York has 7,154), its government and regulatory focus cannot compete in terms of the fee income and high-margin mandates that emanate from the corporate and finance hotspot that is London.

Data in The Lawyer’s inaugural Global 200 confirms the longstanding impression that when it comes to the global legal market’s beating heart, it lies on the professional services trade route between Manhattan and the City.

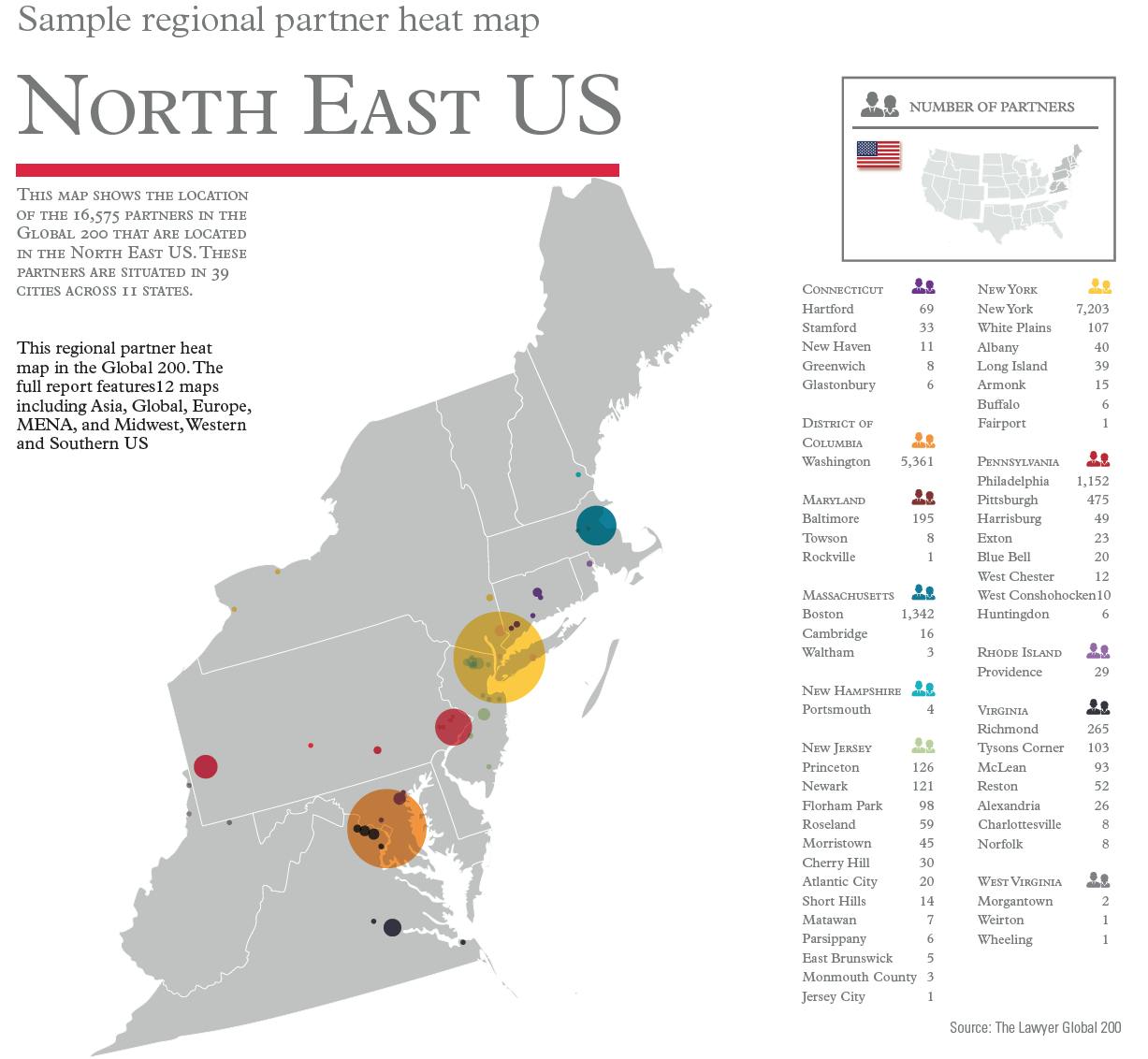

To put the sheer scale of the New York-London (NYLon) axis into context, of the 571 cities included in The Lawyer’s Global 200, about 300 have fewer than 10 partners based in them and just 13 have more than 1,000.

Only three – New York (7,154), London (5,347) and Washington DC (5,355) – have more than 5,000 partners, with Chicago and Los Angeles chipping in with 3,493 and 2,370, respectively.

New York and London together contribute 20 per cent of the total of 62,884 partners in the Global 200, and the lawyers in the two cities increasingly share the spoils from the world’s top clients.

The data confirms that, despite the significant investments made by numerous firms into markets such as Asia-Pacific and elsewhere, for many internationally focused firms the NYLon axis remains the most critical.

To buy the full, 200-page Global 200 report, contact Richard Edwards on richard.edwards@thelawyer.com or 020 7970 4672

Wealth of data

This is reinforced by a wealth of data in the Global 200 report. Notably, while there may be more Global 200 firms in total with a presence in New York than in London, the number of firms with a significant presence in both cities in terms of partner numbers are remarkably similar.

Seventeen Global 200 firms have 100 partners or more in New York, compared with 18 firms with more than 100 partners in London.

At the other end of the scale, there are 14 firms with fewer than 10 partners in New York, but 40 firms with fewer than 10 in London.

“Of the Global 200 firms, 138 have an office in New York”

Now, let’s get granular. Of the 93 firms that are present in both cities the average size of the total group of partners in the office is 59.4 in New York and 37.2 in London.

On a practice area basis, the average number of corporate group partners is 16.6 in New York and 10.2 in London.

Predictably, New York dominates when it comes to litigation, with an average group size of 15.8 partners compared with London’s 6.1, whereas finance teams are virtually identical (5.8 in New York, 6.6 in London).

Real estate teams on both sides of the Atlantic are also of a similar size, and consistently smaller, at 3.2 in New York and 2.6 in London.

All four of these areas, although by no means exclusive to the NYLon market, are in most cases where the centre of gravity of the world’s biggest clients lies. No wonder the size of firms’ teams is significant.

Key areas of investment

These practice area statistics highlight the key areas of investment for the world’s largest firms. At a macro level, for an increasing number of firms the strategic Holy Grail is simply achieving critical mass (including supporting practices) in both London and New York.

Clearly, for as long as there has been cross-border work the NYLon axis has been critical. But over the past couple of years, there have been signs that several factors have raised the strategic imperative to be viable in both cities to an unprecedented level.

In particular, regulatory and investigations-related work along this axis has boomed, with dozens of firms scrambling to hire top talent and lay claim to that space.

Economically, the US legal market has become relatively stagnant in the past couple of years so the country’s firms are looking for ways to get the engines firing again.

And even for US firms that are already present in both the US and the UK, there is evidence that the highest bonuses and salaries are coming from practices focused on either London or New York, or both (see Cravath Swaine & Moore’s recent benchmark-busting pay rises that were immediately matched by NYLon rivals).

All these factors are conspiring to make this legal market fault line the most in-demand in the world. But The Lawyer’s data confirms there is a long way to go before any single firm can claim to dominate this market.

UK firms losing ground

Only two firms that might be classed as at least significantly UK-headquartered – DLA Piper and Hogan Lovells – feature in the New York top 50 ranking in the Global 200 (in which firms are ranked by the total number of partners based in the city). In fact, there are signs that the UK firms are losing ground to their US rivals.

While none of the four magic circle firms make it into the New York top 50, a total of 17 US-headquartered firms – Akin Gump, Baker & McKenzie, Dechert, Dentons, Jones Day, Kirkland & Ellis, K&L Gates, Latham & Watkins, Mayer Brown, Morgan Lewis, Reed Smith, Ropes & Gray, Shearman & Sterling, Sidley Austin, Squire Patton Boggs, Weil Gotshal & Manges and White & Case – feature in the London top 50.

This underlines the long-held impression that it is harder for UK firms to crack New York than it is for US firms to cross the Atlantic and make inroads into the City.

However, both routes require significant investment, single-minded leadership and partnership buy-in. In a nutshell, breaking either city isn’t easy – or cheap. Nor is a merger necessarily the best option. The fact that in recent weeks talks between Berwin Leighton Paisner and Greenberg Traurig, and also reportedly Arnold & Porter and Kaye Scholer have come to nothing underlines how problematic securing a merger can be. This impression was further underscored by Bond Dickinson and Womble Carlyle’s deal being structured as an alliance, not a merger.

Increasingly for many firms looking to build capabilities in both New York and London, the way to do it is via targeted, cherry-picking lateral hires. But that is easier said than done. First off, US-based legal recruitment consultant Joe Macrae of Mlegal believes US law firms that intend to make a serious bid to grow in London need enough revenue to support substantial investment.

“For some firms in the $300m-$500m (£200m-£350m) revenue bracket, the challenge is how to manage the competing priorities of not diluting profits and not incurring significant debt,” says Macrae. “The post Dewey/Thelen/Brobeck world is one where firms are often keen to stress to laterals that they have ‘zero debt’ or ‘close to zero debt’, so the idea of even modest borrowings can be somewhat problematic.”

Certainly, some of the headline costs of launching an office can mount up. They include lawyers’ salaries and partner payments (potentially $2m apiece or more); office rent; insurance; travel costs of flying partners from the US to London (generally business class) and decent hotels to put them up in, plus ongoing visits as the office beds in; and, of course, recruitment and other consultants’ fees.

“It is by no means stretching it to say that investment in a relatively small group of hires could cost you $5m to $10m or even more in the first year,” says Macrae. “Depending, of course, on the size of the firm, that can easily translate into a cut in unit value at the firm of several percentage points for every partner.”

Then you have to hope the clients pay.

“It’s almost always the case that there is a 30- to 90-day lag before partners start collecting fee income, assuming everything goes as well as predicted,” adds Macrae. “It’ very easy to find yourself in a situation where you rack up millions of accumulated cost before a single dollar comes in the door.”

It is likely that for partners in the fiercely competitive and dollar-focused legal market of New York in particular, going home and saying “I’m taking a 10 per cent hit for the good of the firm” is something remarkably few are willing to do.

“Saying ‘sorry, we can’t afford the country club this year’ tends not to go down well,” says Patty Morrissy, also of Mlegal in the US. “People very quickly become accustomed to the style they are living in.”

Cracking London

There are signs that, just as UK firms have learned how tough it is to break Manhattan – although that has not stopped them trying – several US firms have learned that cracking London is also a lot easier said than done.

A growing number of firms that have been in the UK for several years, including McDermott Will & Emery, Morrison & Foerster and Winston & Strawn, have recently overhauled their City strategies to raise their profiles in London.

Others have made much more visible – and opportunistic – plays. One of the biggest deals in recent years was Akin Gump’s effective takeover of Bingham McCutchen’s London office, a deal that catapulted it up the rankings of the largest US firms in the City and gave it a much more robust global platform, with New York and London a key part.

Bingham’s financial restructuring practice, which is strong on the creditor side, coupled with Akin’s energy brand was compelling, particularly in the context of plummeting fuel prices, while the City additions boosted the firm’s Moscow, London and Houston axis. It also provided a launch pad for Akin to pursue the expansion of its energy practice in Asia.

As we reported in last week’s feature, other firms have, as they put it, pressed reboot and looked to re-energise their London offices. Take Katten Muchin Rosenman. Its UK strategy has been stop-start for several years, stretching back to the early Noughties under previous managing partner Martin Cornish, who left the firm for K&L Gates in 2011 and is now a partner at boutique MJ Hudson.

Katten’s new global managing partner since 1 June this year, Roger Furey, confirms: “London forms a key part of our strategic direction as it is the gateway to Europe. We will be investing time and capital in growing our office and offering there.”

Furey, who says the firm has been working on “rebooting” the practice since the 2012 hire of Mayer Brown’s former head of real estate Peter Sugden, points out that part of the issue facing Katten a decade ago was simply the economic environment. The days of the boom in funds formation work around 2005 trailed off into the financial crisis in 2007 and 2008.

Furey also concedes that 10 years ago the firm’s core line of business “was more novel”, but rapidly became more commoditised. A decade on, and he says the key to Katten’s future success will be to stay strategically focused.

“We don’t want to be doing everything in London,” he says. “We learned some lessons the hard way, but Peter brings us that ability to find the right quality of lawyers in strategic areas.”

For Katten, that means real estate and financial services, two of its cornerstone areas firmwide, with 55 and 71 partners respectively, according to the Global 200.

“We will be building out in these two practices, but also in support areas such as corporate, tax, employment, litigation and construction,” says Furey. “Our sell is that this is a law firm that is serious about its financial services and real estate practice. We’ve shown our ability to invest in other cities; now we’re going to show it in London.”

Premium markets

As we report in the Global 200, many of the leading international firms are building along the NYLon axis because they have leveraged off premium markets in the City and Manhattan. The further a firm is away from those markets, the less likely it is to be one of the big-revenue suppliers of legal services.

The clearest recent example of this is in private equity, where there has been a scramble in the City to acquire the best talent (and contacts books) available.

Simpson Thacher & Bartlett, in particular, has created a fair bit of swagger in recent years off the back of its booming funds and deals practice. With US clients such as Blackstone and KKR anchoring the practice, this is evidence that if firms offer a one-stop-shop service with the right talent (which means English and US law capabilities with the right level of quality in the right areas) most clients will buy it.

The problem, as Macrae points out, is that sometimes this rationale is either less clear-cut or a firm simply has not nailed it down strategically.

“Just because a firm has a relationship with a client in the US doesn’t necessarily mean it will use you if you open an office in London,” he says. “I’ve been surprised by the number of firms that fail to ask clients the basic question: what does our team need to look like in London for us to be in a position to dislodge your London advisers?”

It’s a simple question, but then some of the most effective things are the most obvious.

How international are practice areas?

As well as looking at how international individual firms are, it is also possible to segment the Global 200 data to determine how international different practice areas are. In other words, we can determine how many partners in any given practice area are based outside their firms’ home jurisdiction.

In terms of sheer numbers, corporate is the practice area with the most partners based outside firms’ home jurisdiction. A total of 1,557 corporate partners work away from their firms’ headquarters, representing 28 per cent of all corporate partners.

However, projects and infrastructure is proportionally the most international practice area. A total of 147 projects partners, or 38 per cent of the total of 389, work outside their home jurisdictions. Banking and finance, where 544 of 1,603 (34 per cent) of partners work in countries outside their firms’ headquarters, is the second-most international practice area.

The practice area which employs most partners in their headquarters is litigation. Of the 6,811 litigation partners tracked by the Global 200 only 864 (11 per cent) work outside their home jurisdiction. Intellectual property (IP), with 86 per cent of partners based in firms’ home jurisdictions, and insolvency, with 83 per cent of partners staying close to home, is the next most-domestic practice area.

Corporate is the most international

DLA Piper has the most international corporate group. A total of 89 per cent of its 405 corporate partners work outside the UK (considered to be the firm’s home jurisdiction for the purposes of the Global 200).

In a further five firms more than 80 per cent of corporate partners are based outside the home country – Baker & McKenzie, CMS, Dentons Hogan Lovells and Norton Rose Fulbright.

A total of 51 firms have corporate groups where 28 per cent (the average for this practice area) or more of the partners work outside their home countries. Meanwhile, a total of 61 firms have entirely domestic corporate practices with no partners overseas.

Most international practice areas

Litigation

DLA also has the most international litigation group, again with 88 per cent of its litigation partners outside the UK. Norton Rose Fulbright and Hogan Lovells are the only other firms with more than 80 per cent of their litigation partners based outside their home jurisdictions.

CMS, Allen & Overy, Taylor Wessing and Ashurst also have large international litigation teams, with between 71 and 79 per cent of their contentious partnerships based outside their home jurisdiction of the UK.

A total of 56 firms have teams of litigation partners which are as or more international than the average of 11 per cent. Underlining the domestic nature of many disputes, 87 firms have no litigation partners at all outside their headquarters jurisdictions.

Bakers most global for banking and finance

Baker & McKenzie has by far the most international banking and finance group of any firm. A total of 135 finance partners out of 153 (88 per cent) are based outside the US, Bakers’ home jurisdiction. That puts the firm 13 percentage points clear of its closest rivals in this metric, Dentons and Norton Rose Fulbright. At both firms three-quarters of banking partners are based outside their home countries. DLA Piper is close behind with 74 per cent of its finance partners based overseas.

Only 48 firms have a banking practice as or more international than the average, which is 33 per cent of partners based away from their headquarters. Meanwhile 74 firms have a wholly domestic banking team.

Real estate, construction and environment

Slater & Gordon has, proportionally, the largest real estate team outside its home jurisdiction of Australia. All but one of its 12 real estate partners are based elsewhere (92 per cent).

Bakers also has a sizeable non-domestic real estate practice. A total of 65 real estate partners are based outside the US, compared to eight in the US (89 per cent).

White & Case (88 per cent), Norton Rose Fulbright (83 per cent) and King & Wood Mallesons (84 per cent) also fall in the group that has 80 per cent or more when it comes to real estate.

A total of 51 firms have at least 15 per cent of their real estate partners based outside their home jurisdictions – the average for this practice area. On the other hand, 111 are entirely domestic in this practice area.

Employment, pensions and benefits

Excluding Kaye Scholer, which has a small, entirely international employment team, Norton Rose Fulbright is the most international in this practice area. Almost all (95 per cent) of its employment partners are outside the UK, or 70 out of 74.

Ashurst also features high up the employment rankings with 85 per cent of its partners outside its home jurisdiction. Meanwhile, Hogan Lovells has 79 per cent of their employment partners outside the UK. A further six firms – Bakers, Bird & Bird, CMS, Dentons, DLA, Taylor Wessing and White & Case – also have more than 70 per cent of their employment partners away from their home countries.

Employment is one of the most domestic practice areas and 113 firms had all their employment partners in their home jurisdictions.

Intellectual property

A total of six firms, including some with quite large IP practices, have no IP partners in their home jurisdictions – Ashurst, Clifford Chance, Clyde & Co, Cuatrecasas Gonçalves Pereira, Kennedys and Slater & Gordon.

A further three are overwhelmingly international in this practice area. At Norton Rose Fulbright 95 per cent of the firm’s IP partners are outside the UK; 93 per cent of Hogan Lovells’ IP team is international; and 92 per cent of Osborne Clarke’s.

However, IP is a fairly domestic practice area and only 22 firms have more than 50 per cent of their IP teams outside their home jurisdictions. In contrast, 116 have all their IP partners in their headquarters.

Sample firm profile – Latham & Watkins

Latham & Watkins may have ramped up its Asian presence, but in partner coverage, the firm is still very much a US player.

Of its 649 global partners, 456 (70 per cent) are based in the US. Of those, 106 (16 per cent) are in New York, 92 (14 per cent) are based in Washington DC and 69 (11 per cent) work out of Los Angeles. The firm’s next largest office is its 67-partner London base, which last year generated the highest turnover of any overseas-headquartered firm in the UK.

Of its 649 global partners, 456 (70 per cent) are based in the US. Of those, 106 (16 per cent) are in New York, 92 (14 per cent) are based in Washington DC and 69 (11 per cent) work out of Los Angeles. The firm’s next largest office is its 67-partner London base, which last year generated the highest turnover of any overseas-headquartered firm in the UK.

Latham added seven private equity and leveraged finance partners in Hong Kong, which is now home to 16 partners, and announced plans to open a foreign legal consultant office in Seoul. The South Korean practice will have an emphasis on banking and finance, which is the firm’s third largest practice worldwide. In total 65 partners are banking and finance specialists, although that number is dwarfed by the 277 working in corporate. At 44 the largest crop of corporate partners are based in New York, 34 in London and 26 in DC.

Litigation and disputes has 143 partners in total. It is largely US focused, with 123 (87 per cent) partners. Washington has the largest team with 37 partners, followed by Los Angeles (19) and New York (18).